How to Calculate PVIFA in Excel

If you want to know what a stream of equal future payments - such as a pension, a bond’s coupon stream, or a loan’s remaining installments - is worth in today’s money, the Present Value Interest Factor of an Annuity (PVIFA) gives you the multiplier you need. Multiply it by the per-period payment and you get the present value of the full stream. It is a core tool in loan amortization, bond pricing, and lump-sum-vs.-annuity comparisons, and Excel can compute it in a single cell.

This guide walks through what PVIFA represents, the closed-form formula, how to type it into Excel, how to cross-check the result against Excel’s built-in PV function, and the one subtlety - ordinary annuity vs. annuity due - that trips most people up.

What Is PVIFA?

PVIFA is the present value, today, of $1 received at the end of each of the next periods, assuming a constant per-period discount rate .

Because it is defined on a $1 payment, it is a pure multiplier. If you know the PVIFA for a given rate and horizon, the present value of any equal-payment stream at that rate and horizon is simply:

This is what makes the factor useful: compute it once for a given pair, then plug in whatever payment size you want. Any equal-payment cash-flow stream with the same rate, timing, and term shares the same PVIFA; only the payment amount changes the final present value.

Two things to pin down before using it:

- The rate and the period must match. If payments are monthly, is the monthly rate and is the number of months. If they are annual, both are annual. Mixing them is the single most common mistake.

- PVIFA assumes payments are made at the end of each period. This is the “ordinary annuity” convention, which fits most loans and bond coupons. If payments are made at the beginning of each period (an “annuity due”), the factor is slightly larger, by a factor of . We cover this below.

The PVIFA Formula

The closed-form expression is:

Where:

- is the discount rate per period (e.g., 4% per year as

0.04, or a 4% stated annual rate converted to a monthly rate as0.04/12). - is the number of periods.

The intuition is straightforward: each future $1 payment has its own PVIF, namely for the payment in period . PVIFA is simply the sum of those PVIFs over all periods. Summing that geometric series gives the closed form above.

A useful way to think about it: PVIFA is bounded above by . As goes to infinity, the formula collapses to , which is the present value of a perpetuity paying $1 forever. So at a 4% rate, no matter how long the annuity runs, its PVIFA can never exceed . That ceiling also helps explain why extending a long payment stream often changes present value less than people expect.

Calculating PVIFA in Excel

The Data You Need

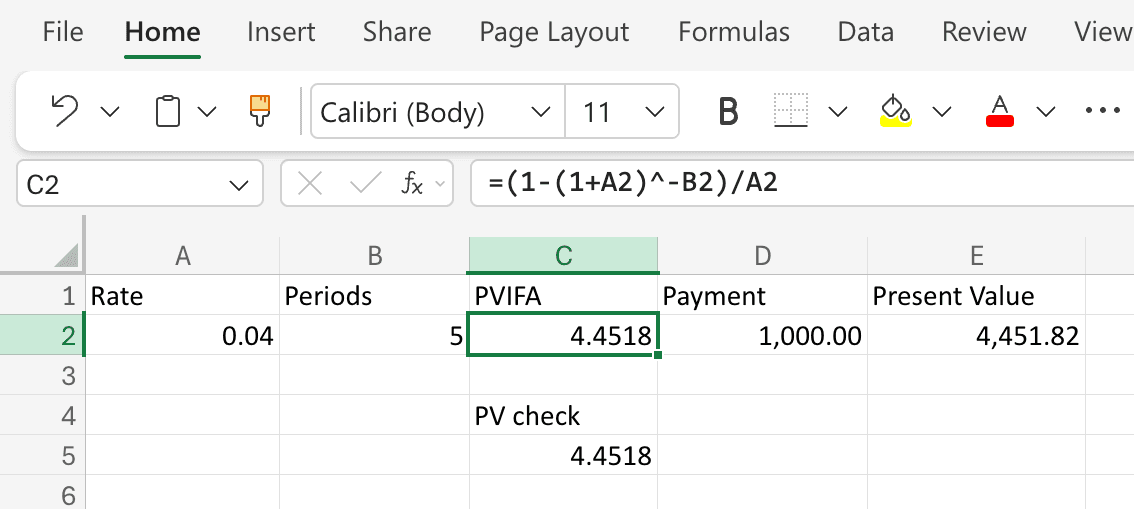

All you need is two numbers: the per-period rate and the number of periods. Lay them out like this:

| Cell | Contents |

|---|---|

A1 | Rate |

A2 | 0.04 |

B1 | Periods |

B2 | 5 |

C1 | PVIFA |

C2 | (formula here) |

Step-by-Step

- Type the rate in

A2. If you want an annual rate of 4%, enter0.04. If payments are monthly at a stated annual rate of 4%, enter=0.04/12instead - the rate must match the payment frequency. - Type the number of periods in

B2. For a 5-year annual-payment plan, enter5. For a 5-year monthly plan, enter=5*12. - In

C2, type the PVIFA formula:

Press Enter. For=(1-(1+A2)^-B2)/A2r = 0.04andn = 5, Excel returns4.4518(to four decimal places). That is the PVIFA. - Optional: compute the present value of an actual payment stream. In

D1typePayment, inD2enter the payment amount (say1000). InE1typePresent Value, and inE2enter:

Excel returns=C2*D24451.82, meaning $1,000 received at the end of each year for 5 years at 4% is worth about $4,451.82 today.

Cross-Checking With Excel’s PV Function

Excel’s built-in PV function can also compute the present value of an annuity directly, which makes it a useful cross-check for your PVIFA formula.

In C4 type a label like PV check, and in C5 type:

=-PV(A2, B2, 1, 0, 0)

The arguments are:

rate- the per-period rate, same asA2.nper- the number of periods, same asB2.pmt- the payment per period. Enter1(PVIFA is defined on a $1 payment).fv- future value,0because there is no balloon payment beyond the annuity.type-0for an ordinary annuity (payments at the end of each period). Use1for an annuity due.

The leading minus sign flips Excel’s cash-flow sign convention so the result comes back as a positive factor. This should return 4.4518 - the same PVIFA you computed from the closed-form formula. If the two differ, you almost certainly have a rate/period mismatch or an annuity-due setting to track down.

Ordinary Annuity vs. Annuity Due

The standard PVIFA formula assumes payments occur at the end of each period (an “ordinary annuity” - most loans and bond coupons work this way). If payments instead occur at the beginning of each period (an “annuity due” - rent, many insurance premiums, some lease payments), every payment is received one period earlier, so each is discounted one less time. The factor becomes:

In Excel, you can either multiply your C2 formula by (1+A2):

=(1-(1+A2)^-B2)/A2*(1+A2)

or let the PV function do it by setting the type argument to 1:

=-PV(A2, B2, 1, 0, 1)

For r = 0.04 and n = 5, the annuity-due PVIFA is 4.6299 - about 4% larger than the ordinary version, exactly one period less of discounting.

A Worked Example: A Lottery Lump Sum vs. Annuity Choice

Suppose you win a lottery that offers two payout options: $1,000,000 today, or $75,000 per year at the end of each of the next 20 years. Assuming you can earn 5% on a comparable-risk investment, which is worth more today?

- Rate per period:

0.05 - Periods:

20 - PVIFA:

- Present value of the annuity:

At a 5% discount rate the lump sum ($1,000,000) is worth about $65,000 more today than the annuity. If you can only earn 3% on safe investments, recompute with r = 0.03:

- PVIFA:

- Present value of the annuity:

Now the annuity wins by about $115,000. The decision flips entirely on the discount rate, which is exactly why PVIFA-based comparisons should always include a sensitivity check on the rate.

Common Mistakes

- Rate/period mismatch. Using an annual rate with a number-of-months period count is the single most frequent error. If payments are monthly, divide the stated annual rate by 12 and convert the horizon in years into months as well.

- Entering the rate as a whole number.

4instead of0.04will give a nonsensical answer. Excel’s percentage formatting on the cell does not change what you type. - Forgetting the annuity-due adjustment. Rent and many insurance products are annuities due, not ordinary annuities. Using the ordinary-annuity PVIFA understates the present value by a full period of discounting.

- Confusing PVIFA with PVIF. PVIF discounts a single future cash flow; PVIFA discounts a stream of equal payments. PVIFA is the sum of PVIFs over all the periods in the annuity.

- Mixing nominal and real inputs. PVIFA is mechanical - it does whatever you tell it to do with the rate. The judgment question is which rate. Discount nominal cash flows with a nominal rate, real cash flows with a real rate; don’t mix them.

Frequently Asked Questions

What is the difference between PVIFA and PVIF?

PVIF discounts a single future cash flow back to today. PVIFA discounts a stream of equal future cash flows. Mechanically, PVIFA(r, n) = PVIF(r, 1) + PVIF(r, 2) + ... + PVIF(r, n) - it is just the sum of the per-period PVIFs.

What is the difference between PVIFA and Excel’s PV function?

They compute the same thing, but PV is an all-in-one function that takes a payment amount directly and returns the present value, while PVIFA is just the multiplier for a $1 payment. If you only need one answer, PV is faster. If you want to apply the same factor to several different payment sizes - for example, comparing several loan offers with the same rate and term - computing PVIFA once and multiplying is cleaner.

Is PVIFA the same as a bond price?

Almost. A standard coupon bond’s price is PVIFA(r, n) * Coupon + PVIF(r, n) * Face Value - the present value of the coupon stream (an annuity) plus the present value of the face value repaid at maturity (a single future cash flow). PVIFA is one of the two building blocks of bond pricing; PVIF is the other.

What happens when the rate is zero?

The closed-form formula has r in the denominator and is undefined at exactly r = 0. In that edge case, PVIFA is simply the number of periods n - because with no discounting, $1 received each period for periods is worth exactly today. Excel’s PV function handles this correctly; the algebraic formula requires a special case.

Can I use PVIFA for irregular payments?

No - PVIFA assumes equal payments each period. If your payments vary, you need to discount each one individually with its own PVIF, or use Excel’s NPV function on an explicit cash-flow column.

Why is PVIFA bounded above by 1/r?

Because as the number of periods goes to infinity, the term goes to zero, and the formula collapses to . That limit is the present value of a perpetuity - a $1 payment forever. So no annuity, no matter how long, can ever be worth more in PVIFA terms than a perpetuity at the same rate. This is also why extending a very long payment stream often changes present value less than people expect.